While medtech over the past five years has seen continued pressure on prices, increased oversight on physician-manufacturer relationships, reduced med/surg procedure volumes, continued regulatory challenges and the real or perceived negative impacts of the Affordable Care Act, the business of spine surgical technologies remains one of the most steadfast oases of innovation and price stability.

The continued growth of spine surgery owes itself to a number of key drivers:

While medtech over the past five years has seen continued pressure on prices, increased oversight on physician-manufacturer relationships, reduced med/surg procedure volumes, continued regulatory challenges and the real or perceived negative impacts of the Affordable Care Act, the business of spine surgical technologies remains one of the most steadfast oases of innovation and price stability.

The continued growth of spine surgery owes itself to a number of key drivers:

- The aging population worldwide

- Increasing incidence of obesity

- A growing middle class in developing countries, with the ability to pay out of pocket for spine surgery

- Improving worldwide economy

- Technological device enhancements, leading to improved surgical results

- Developments in minimally invasive spine surgery (MISS) devices driving a strong increase in MISS, with its numerous advantages

- In the US, improvements in reimbursement as clinical trials demonstrate the efficacy of treatments using the devices

- US healthcare reform leading to medical insurance coverage for more people, allowing those suffering from intractable back pain to receive surgical treatment

(The last, of course, is debatable, since medical device manufacturers are not yet convinced that a 3.2% excise tax is supported by the anticipated boost in patient population. The jury is still out on this and, in any case, prospects for the 3.2% tax being repealed are slim, despite repeated efforts.)

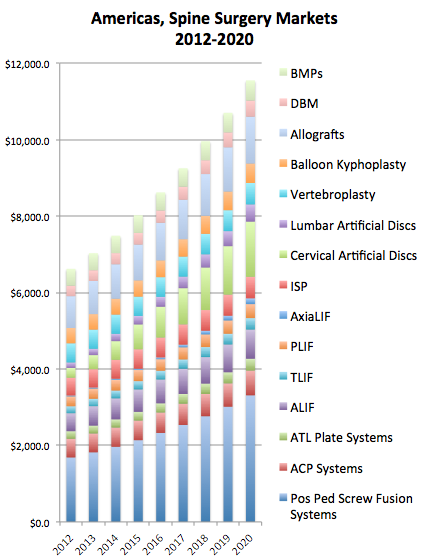

Consequently, the worldwide aggregate spine surgery market has a 2012 to 2020 compound growth rate of 7.7%, with individual segments within it growing at a low of 2.3% to a high of 35.0%.

It is also worth noting that we have identified seven (7) new medtech startups in spine surgery that have been founded in the past three years alone.

Below is illustrated the spine surgery markets in the Americas and Europe for 2012-2020.

Source: MedMarket Diligence, LLC; Report #M520, “Worldwide Spine Surgery: Products, Technologies, Markets and Opportunities 2010-2020″.