This post was written by Tom Saving and me and originally appeared at the Health Affairs blog.

Of all the issues bandied about in the recent debate over the debt ceiling, none generated more contention, more TV ads and more unseemly rhetoric than potential changes to Medicare.

This post was written by Tom Saving and me and originally appeared at the Health Affairs blog.

Of all the issues bandied about in the recent debate over the debt ceiling, none generated more contention, more TV ads and more unseemly rhetoric than potential changes to Medicare.

Health economists generally believe that Medicare is on an unsustainable course and is desperately in need of reform. Yet public opinion polls show that most seniors disagree. They not only resist cuts in Medicare to solve the problem of federal deficit spending, they also resisted the spending cuts and delivery of care innovations envisioned by the Affordable Care Act (ACA), as well as the private insurance innovations envisioned by Rep. Paul Ryan (R-WI) and the House Republicans.

In short, most seniors would like to keep Medicare just like it is.

A similar view is held by a small, but vocal group on the left that favors single-payer national health insurance. The Physicians for a National Health Program, for example, claims that Medicare has lower administrative costs than private insurance and is able to use its monopsony (single-buyer) power to suppress provider fees. The group, which is resistant to managed care, favors “Medicare for all” and endorses a bill to do just that by John Conyers.

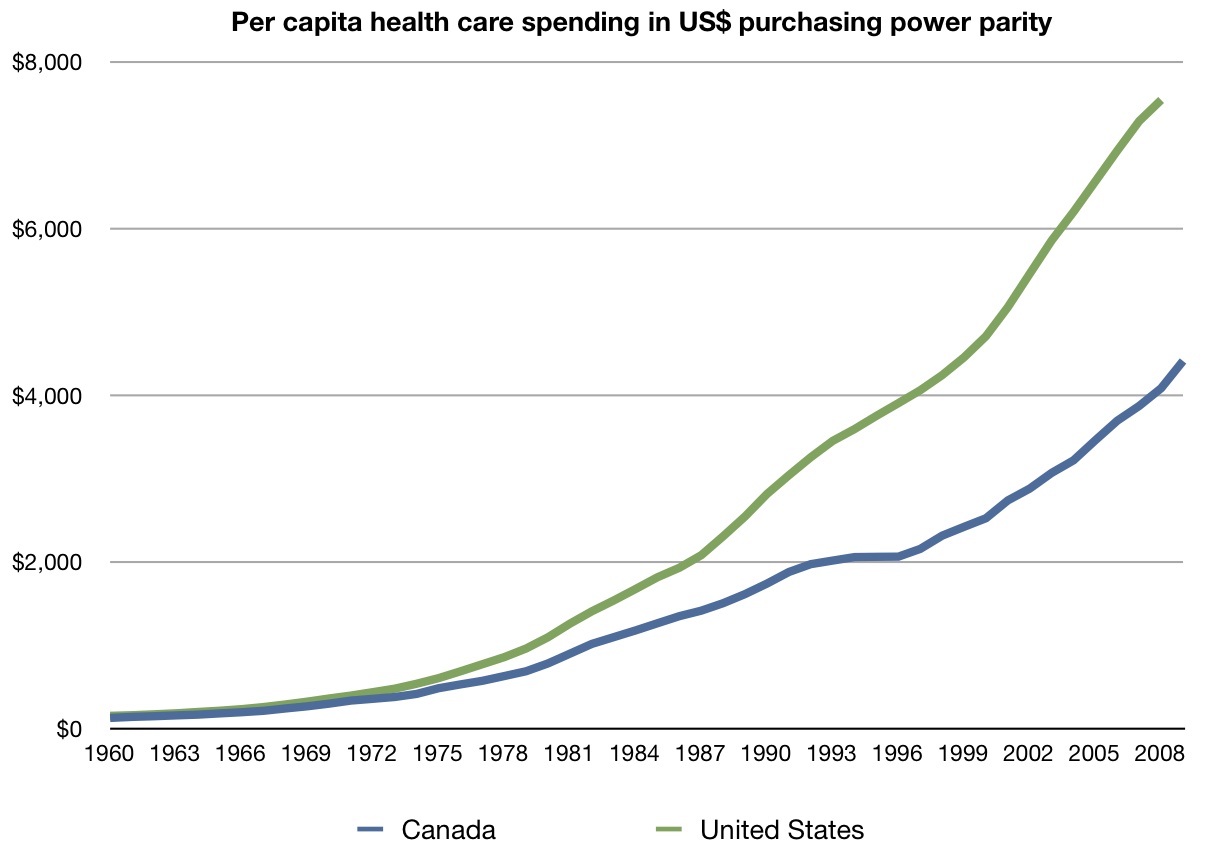

Paul Krugman, writing in The New York Times, also argues this way. He points to a chart (see Figure I) which seems to show that Medicare per capita spending is growing at a slower rate than private insurance. Krugman, along with others, touts the slower rate growth in the Canadian health care system (also called “Medicare”). In recent editorials, both Krugman and Robert Reich have joined the call for Medicare for everyone.

Are these unconventional critics right?

Let’s begin with a fundamental point that almost everyone tends to ignore. Medicare is not actually managed by the federal government. In most places it is managed by private contractors, including such entities as Cigna and Blue Cross. To argue that Medicare is more efficient is tantamount to arguing that when Blue Cross is called “Medicare” it is more efficient than when it is called “private insurance.” Further, there is nothing particularly special about the way Medicare pays providers. Private insurers tend to use the same billing codes and their payment rates are often pegged as a percentage of Medicare rates.

Claim Of Lower Medicare Administrative Costs Is Based On An Incomplete Comparison

What about the claim that Medicare’s administrative costs are only 2 percent, compared to 10 percent to 15 percent for private insurers? The problem with this comparison is that it includes the cost of marketing and selling insurance as well as the costs of collecting premiums on the private side, but ignores the cost of collecting taxes on the public side. It also ignores the substantial administrative cost that Medicare shifts to the providers of care.

Studies by Milliman and others show that when all costs are included, Medicare costs more, not less, to administer. Further, raw numbers show that, using Medicare’s own accounting, its administrative expenses per enrollee are higher than private insurance. They are lower only when expressed as a percentage — but that may be because the average medical expense for a senior is so much higher than the expense for non-seniors. Also, an unpublished ongoing study by Milliman finds that seniors on Medicare use twice the health resource as seniors who are still on private insurance, everything equal.

Ironically, many observers think Medicare spends too little on administration, which is one reason for an estimated Medicare fraud loss of one out of every ten dollars of Medicare benefits paid. Private insurers devote more resources to fraud prevention and find it profitable to do so.

Are Medicare Costs Growing More Slowly? No. What about the claim that Medicare’s cost per enrollee is growing more slowly? The problem with the diagram in Figure I is that it ignores the falling share of private out-of-pocket spending over the past 40 years, as the insurance share of the bill escalated and the changing demographic structure of the two populations as the private insured market aged. A more accurate picture is provided by the Congressional Budget Office (Figure II), which makes appropriate adjustments and calculates spending in excess of GDP growth for the public and private enrollee populations. As the figure shows, Medicare has been growing faster than the private sector. For that matter, Medicaid has also been growing faster.

Source: Krugman/New York Times; Centers for Medicare and Medicaid Services

Source: Congressional Budget Office

As the CBO acknowledges, its comparison is far from perfect. The “other” category includes the uninsured as well as out-of-pocket spending by Medicare enrollees. Still, there is no reason to believe that overall spending would have been lower if the entire country had been in Medicare for the past 35 years.

Looking forward, the CBO believes that Medicare will grow more slowly than the private sector. It will grow a lot more slowly if the provisions of the Patient Protection and Affordable Care Act (PPACA) are implemented without any changes. Under the act, Medicare will suppress provider fees so immensely that real per capita Medicare spending will grow no faster than real per capita GDP. Yet the rest of the health care system will be growing at twice that rate. As the Medicare Office of the Actuaries has explained, this means greatly reduced access to care for the elderly and the disabled. As we previously explained, a two tiered system will emerge before this decade is out. Because of the political ramifications of all this, almost no one believes that the PPACA will remain unchanged. Like the so-called “doctor fix,” the Medicare cuts in the law are likely to be restored.

The Argument Based On Government Single-Buyer Market Power: Five Problems

What about the argument that government can use its power as a single buyer to suppress providers’ fees? There are five problems with it.

Health care markets are local. First, we don’t buy health care in a national market. We buy locally. And in local markets, private entities are often as big, or bigger, than Medicare (the auto companies in Detroit, for example, or the mine workers and their employers in West Virginia). There is nothing the US government can do that a lot of private companies and unions cannot also do. Similarly, if Canada is seen as the ideal, nothing is stopping the auto companies and the UAW from creating a global budget and rationing care for auto workers just the way the Canadians do it. That they choose not to do so is telling.

Side effects of suppressing provider fees. Second, there are negative consequences from unduly suppressing provider fees. Doctors can leave the city, the state, or even the country where they live and go elsewhere. Able people can also avoid the profession altogether. If we paid doctors only the minimum wage, for example, medicine would attract only those people who can earn no more than the minimum wage doing something else. The suppression of provider payments ultimately harms patients as highly qualified providers exit the market. The effects of price controls in health care will be similar to their effects in other markets.

Cost-shifting. Third, the suppression of provider payments shifts costs from patients and taxpayers to providers. Shifting costs, however, is not the same thing as controlling costs. Providers are just as much a part of society as patients. Shifting cost from one group to the other makes the latter group better off and the former worse off. It does not lower the cost of health care for society as a whole, however. In fact, it introduces a cost to society as the supply of providers falls.

Political pressures and lobbying. Fourth, the argument overlooks the fact that public insurance in a democracy is ultimately subject to pressures at the ballot box. Providers get to vote too. They also can make campaign contributions and lobby. Patients can also exert political pressure. Political competition in a democracy constrains public policy in much the same way that economic competition constrains the behavior of private firms in the marketplace.

You can get Medicare price controls without Medicare. Finally, if it really were desirable to have everyone pay low prices we do not need to enroll everyone in Medicare to achieve that outcome. We could instead impose Medicare-type price controls on the entire health care system. In fact, one organization advocates that very thing. Doing so would run into all the problems listed above, however.

The Best Medicare Advantage Plans Deliver More Than Traditional Medicare

What about the observation that private sector Medicare Advantage plans are costing the government more than what Medicare would have paid? Some of the “over payments” represent Congressional interference (e.g., the desire to make sure the plans serve rural areas) and some represent poor administration of the program. A more basic issue, however, is that these plans are not just providing Medicare services. They are also providing a less expensive, more efficient form of medigap coverage — mainly to low-income seniors who could not otherwise afford supplemental insurance. If we are indifferent about whether seniors have this insurance, that is one thing. But if we are going to insist that everyone have it, integrated private plans are probably much superior to more subsidies for the current Medicare/medigap arrangement.

For our purposes, the most interesting characteristic of Medicare Advantage plans is that many of them are already doing what the Obama administration says it wants to do with Medicare as a whole — without any prodding or nudging from the federal government. That is, many of these plans are using coordinated/integrated/managed care systems to achieve fewer admissions, fewer readmissions and fewer hospital days than conventional Medicare. By contrast, the Obama administration’s plan to encourage Accountable Care Organizations is so bogged down in bureaucratic rulemaking that our most cost effective health organizations are refusing to participate.

On Innovation, Medicare Follows Rather Than Leads

What about the argument that Medicare is needed in order to spur doctors to practice medicine efficiently? As in the case of Medicare advantage plans, all too often, Medicare is a follower, not a leader, on the innovation front. It is more likely to slow things down than to speed things up. What spurs private firms to be efficient is competition for consumers, not regulation.

In health care, many private sector entities are already doing what the administration says needs to be done:

- Concierge doctors are consulting by email and telephone, keeping electronic medical records (EMRs), prescribing electronically and offering same day or next day appointments.

- Walk-in clinics are posting (transparent) prices, using evidenced-based medicine by following computerized protocols, and keeping EMRs as well.

- Cosmetic and Lasik surgeons routinely offer “bundled” prices, compete for patients based on price and quality and have lowered the real price of their services over the past decade.

- There are lots of successful examples of coordinated care, integrated care, managed care, medical-home care and home-based care (see, for example, here) — almost all of it developed despite Medicare incentives not to do so and in some cases saving Medicare millions of dollars without any compensation.

Genuine reform would seek ways to encourage more such private sector activity. The Ryan proposal would allow a more flexible and robust Medicare Advantage program, in which health plans would compete on price and quality for patient dollars.

{kind=link}