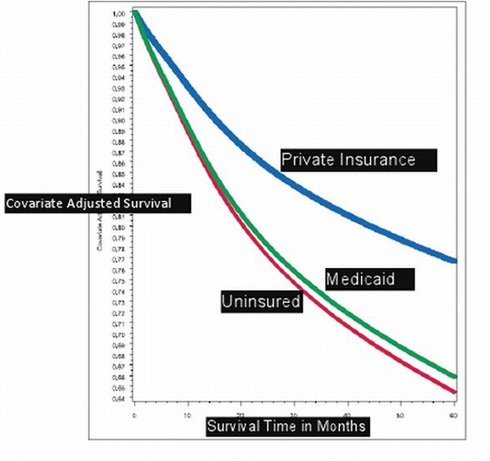

The graph below shows cancer survival rates by patients, depending on their health insurance status. It was posted last Thursday by Sarah Kliff, who says she got it from Zeke Emanuel, the former White House health advisor who helped shape the Affordable Care Act (ObamaCare).

The graph below shows cancer survival rates by patients, depending on their health insurance status. It was posted last Thursday by Sarah Kliff, who says she got it from Zeke Emanuel, the former White House health advisor who helped shape the Affordable Care Act (ObamaCare).

I haven’t seen the study and it may not withstand scrutiny. It seems to contradict the economics literature, which finds that health insurance has very little impact on mortality. But since it comes from “the other side” so to speak, I am going to take it as valid for present purposes.

I haven’t seen the study and it may not withstand scrutiny. It seems to contradict the economics literature, which finds that health insurance has very little impact on mortality. But since it comes from “the other side” so to speak, I am going to take it as valid for present purposes.

What do you conclude by looking at this chart? My answer is below the fold.

More Read

We are about to spend $1.8 trillion over the next ten years insuring about 32 million people. About half of the newly insured will go into Medicaid and half will get private insurance. If the above chart is to be believed, which half you’re in makes a real difference.

That tiny little sliver of difference between the green line and the red line is the differential survival between those who are uninsured and those who are in Medicaid. Even after five years, the differential survival is a little more than 1%.

So why are we spending all that money if the impact on health is so small? It gets worse. The actual additions to the Medicaid population will be much greater than the newly insured. Given the opportunity, many people who currently have private coverage will drop their insurance to take advantage of free insurance from Medicaid. In fact, estimates are that 50% or more of people who become newly eligible for Medicaid will drop their private insurance to take advantage of free government coverage.

That implies that for millions of people we are about to spend billions of dollars and may — after all is said and done — leave them worse off than if we had done nothing at all!

There is more bad news. Many of the people who are newly insured with private coverage will be in health plans that are highly subsidized. We don’t really know what these plans will look like. However, if the Massachusetts model is followed, the subsidized private insurance plans will pay doctors and hospitals only a bit more than Medicaid pays. In other words a good part of the increase in private coverage may be nothing more than Medicaid plus.

And here again, given the opportunity to have free private coverage that pays, say, 10% over Medicaid, many people will drop their standard BlueCross coverage to take advantage of the offer. In so doing they will be giving up coverage that promises a greater chance of survival for coverage that reduces those chances.

The upshot is that the Affordable Care Act may actually lower overall health outcomes for the country as a whole!

You have to wonder why ObamaCare is so rigid. Why can’t people who qualify for Medicaid have the opportunity to opt into private coverage instead. For example, the average amount that Medicaid spends on an adult is about $3,000. The average amount spent on a child is $2,000. So why can’t we give the adults a $3,000 voucher and the children a $2,000 voucher and let them apply these amounts to private insurance premiums instead?

![]()

{kind=link}