In an analysis of last year’s medtech M&A transactions, analysts at New York’s Walden Group Inc., a strategic healthcare investment banking and consulting firm, identified 10 major forces that are shaping medtech:

Market changes. Provider consolidation and the formation of Accountable Care Organization are centralizing care among larger, integrated institutions. They’re also centralizing purchasing power, which usually results in fewer vendors servicing them, Walden says. “For medical device and diagnostic companies, scale and resources will count more in penetrating the hospital space and even non-acute care settings, which too are becoming more inter-connected.”

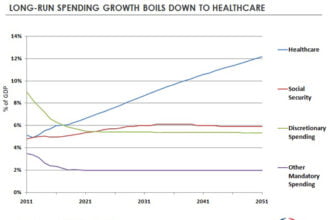

Reimbursement, under pressure. In the transition to bundled payments and value-based care, federal reimbursement for many services is falling. New products that demonstrate better effectiveness and outcomes drive value for payers, but many newer technologies that were expensive to develop won’t make it. Walden cited Shire’s divestiture of its Dermagraft skin substitute line as an example, as Medicare reduced reimbursements for such wound-healing products last year.

Personalized medicine. Using a person’s genetic distinctions diagnose and treat disease and predict susceptibility has opened up new doors for development of interventions that avoid or reduce the extent of a disease for at-risk people. “While development and approval of companion diagnostics has been less than speedy, the growth in companion diagnostics is inexorable,” Walden analysts wrote.

Rise of home care and retail. More care is being delivered outside of hospitals, which has led to recognition among companies that they’ll need more comprehensive solutions that stretch beyond an episode of care.

Data, data, data. Sensors and other data-collection tools are coming to their rescue. St. Jude Medical’s recent acquisition of CardioMEMS, which developed an implantable sensor to more closely monitor patients with heart problems, is one example.

Promising innovations come to market. New technologies that show improvements over current standards of care could potentially change those standards of care. That’s what’s happened with transcatheter heart valves (made by Edwards LifeSciences and Medtronic) for patients who are too old or sick to undergo open-heart surgery.

But not all of them are as great as they initially seem. Medtronic paid $800 million up for Ardian, a company that developed a minimally invasive procedure for drug-resistant hypertension, in 2010. But the procedure recently failed to meet its primary endpoint in its U.S. pivotal trial. Shortly thereafter, Covidien said it would discontinue its OneShot Renal Denervation program.

Cautious optimism for emerging markets. Emerging markets like China, India and Brazil are still fertile ground for opportunities in healthcare innovation, but their “shaky economies and currencies, coupled with unpredictable government and legal systems” are cause for caution, Walden says.

Price challenges for pharma. Despite the quick pace at which new drugs are being launched, a cost-conscious marketplace is causing some high prices to be challenged. “When multiple treatments are available, insurers are more aggressive in steering prescriptions to less-expensive generics,” Walden analysts wrote.

More out-of-pocket payments, less utilization. The growth of streamlined high deductible plans has left more healthcare dollars coming straight out of Americans’ pockets. In many areas of the country, utilization has slowed. If it’s because they’re choosing to forgo screenings or treatments, that could end up causing more problems down the line.

[Image credit: Walden Group]